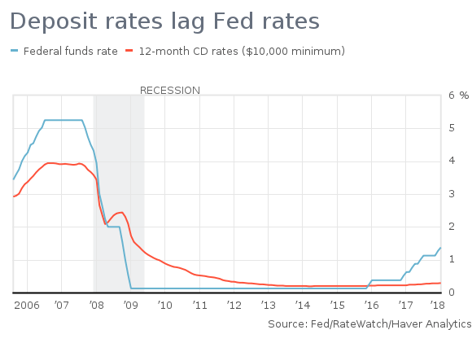

Certificate of Deposits (CDs) are a great way for customers to grow investments over a set term with very low risk. Traditionally, CD rates were higher than they have been in the past 10 years. Longer term CD rates were higher than offered short term rates, but today are not above 2.00% APY on average. In the years before 2008, 5.00% CDs were common, allowing for easy gains on investments. After the financial crisis 10 years ago, the Federal Reserve Bank lowered their interest rate to 0.00%, throwing a damper on all products in the interest market. The length of time interest rates were kept low was far longer than many expected, and hurt the financial institutions consumers.

The interest rate climate is looking a lot better. In 2017 the Fed raised rates three times and we are now sitting at a range of 1.25% - 1.50%. With the forecasted rate increases in 2018 and 2019, the economy and interest rates are starting to look more preferable for banks, credit unions and consumers. But, what effect does this have on CD rates, and how quickly?

When interest rates get a bump from the Fed, be it 0.25% or more, CD and other deposit rates might see an immediate bump, but if they do, it is usually under 5 basis points (0.05%). While only adding the slimmest boost to deposit products, financial institutions add the full 0.25% to their prime lending rate. Greater CD rate increases can be found at online banks that see more competition than the average institution, and must keep up to maintain the deposit pull necessary for lending. Deposit rates aren’t increasing at an equal rate because of the amount of deposits that are on the books and a lack of demand for more by FI’s. Commercial bank deposits totaled roughly $11.99 trillion as of February 2018, more than double what they were in the first half of 2016. Eventually, banks could feel some pressure to increase rates faster if treasury bond rates ever are more than CD rates. Essentially financial institutions are overcapitalized and there is no reason to price compete to increase the supply of money.

Certificate of Deposit rates do increase after the Federal Reserve Bank makes a decision to increase interest rates, but they do not increase to the level of the new set rate. CD rates, and other deposit products, are influenced by the demand for loans more than rate increases. Banks and Credit Unions should keep their competitive market in mind, when increasing CD rates, after a Federal Reserve rate hike. There is an opportunity for increasing goodwill with customers and members by having marginally higher rates versus local competitors. Overall, the increase in offered rates we have seen since 2015 is promising. Hopefully, the rates keep moving towards the 5.00% that were offered pre-crash.

Sources

- http://www.chicagotribune.com/business/ct-fed-rates-marksjarvis-1217-biz-20151216-story.html

- https://www.marketwatch.com/story/savers-havent-benefited-as-the-fed-has-jacked-up-rates-powell-admits-2018-02-27

- https://www.reuters.com/article/us-usa-fed/fed-raises-interest-rates-keeps-2018-policy-outlook-unchanged-idUSKBN1E70IX

- https://www.nerdwallet.com/blog/banking/cds-fed-rate-increase/

- https://www.knoxnews.com/story/money/columnists/david-moon/2017/01/01/moon-loan-rates-not-cd-rates-increase/95910364/

- http://buffalonews.com/2014/07/21/cd-rates-are-barely-budging-from-record-lows/